The fintech industry is growing every year, offering high profitability for products. Therefore, if you are building a product in this industry or considering one in the future, you need to figure out how it will connect to the global financial system. One way to do this is that you could build the connection on your own, which would probably take time and add costs, or you could simply use existing solutions.

The last option plays out well. Through white-label fintech platforms, you could quickly connect your business to pre-built financial products. This means you get to speed up its launch, and your team can focus on other activities that actually move it forward. However, it is important to note that not every white-label fintech solutions provider is built the same. Some excel at banking, others in crypto services, and others in payment gateways.

In this article, we take you through some of the best white-label fintech solutions that represent these different approaches and ones you could integrate with your business.

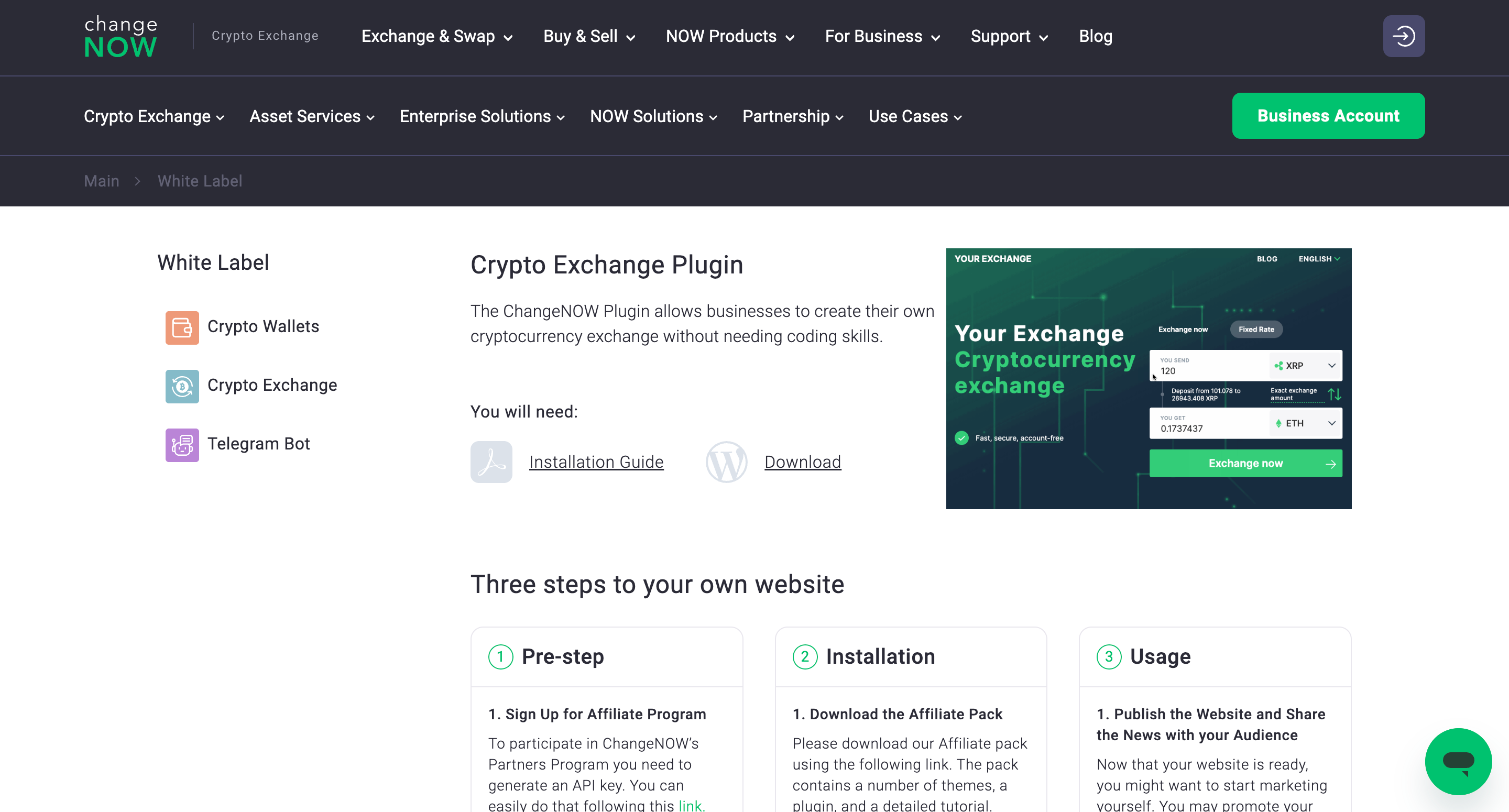

After analyzing all the providers, we have concluded that ChangeNOW is the best white-label fintech solution designed for businesses that want to launch crypto exchange functionalities. Integrating it is made easy via a ready-to-deploy widget or an API with 24/7 team support and a personal manager. Once integrated, your business turns into an exchange platform offering non-custodial crypto swaps across 1,500 cryptocurrencies and support for over 70+ fiat currencies. And the best thing? You get to customize the exchange to match your product needs.

The List of Best Fintech White-Label Solutions:

ChangeNOW

NOWPayments

Rapyd

Gemba

Crassula

AlphaPoint

SDK.finance

Swan

How Do We Select the Best Fintech White-Label Solutions?

When picking the best white-label fintech solutions, we compare providers across three key areas: their revenue model, customization options, and ease of integration. These are what show how well each of them is aligned with your business needs.

Revenue model: We first look at how a white-label generates revenue, either through monthly or yearly subscription fees or upfront fees that businesses pay to integrate it. Then we look at how revenue sharing of the transaction fees generated through the integration is done between the white-label and your business.

Customization Options: The best white-label should allow you to tailor its financial product according to your brand and user experience requirements. This means that you should be able to integrate your brand logo, colours, and messaging to make everything correspond with your business identity. The solution should also provide optimizable language and currency variables, which are important if your product serves international customers.

Ease of Integration: Revenue models and customization capabilities are not enough; the ease of integration also matters. The best fintech white-label should have a variety of APIs and SDKs with clear documentation to facilitate this.

Also, stable technical support is something to check here. You need the best assistance you can get before and after the integration. So, we will check the availability of technical support from each of these solutions.

With this evaluation criterion defined, the following table compares the first five solutions to help you easily identify which one meets your specific business needs:

Provider

Revenue Model

Customization Options

Ease of Integration

ChangeNOW

Detailed revenue-share model (earn 0.4% exchange commissions), staking rewards, and loan interest, customizable transaction fees for specific assets/pairs/flows

Customizable colors, branding, exchange flow, and supported assets

Ready-to-deploy widget or API integration, 24/7 support and personal account manager

Fully white-labeled payment and payout flows under your own branding, domain, and interface

API documentation in 13 programming languages, customizable payment button, active support team

Rapyd

Percentage-based transaction fees plus fixed country/payment-method fees, FX fees on cross-border transfers, recurring commissions based on transaction volume

Customizable UI including themes, fonts, logos, and payment method plugins

REST API integration with comprehensive documentation and technical support

Gemba

Zero setup fees, partners retain up to 70% of custom user fees plus 20% share of base transaction fees

Branding customization through logo uploads, colour palette setup, and custom subdomain mapping

No-code setup with simple DNS configuration

Crassula

SaaS subscription model with recurring monthly/annual fees plus low usage fees, businesses keep profits from custom transaction fees, subscriptions, and FX markups

White-labeled colour schemes, logos, brand styling, plus branded iOS, Android, and web apps

No-code white-label UI via DNS connection or REST API for deeper integration control

The wallet service is meant for businesses to launch a non-custodial cryptocurrency wallet with fiat on-ramping, support for more than 1,500 tokens (700+ of which are available for instant cross-chain swaps), as well as staking and NFT management.

Meanwhile, the exchange feature enables clients to offer cross-chain token swaps for over 1500 crypto assets across 110+ chains to their users. Deploying it requires no code and comes without upfront costs. The Telegram bot, on the other hand, is meant for businesses that want to expand into Telegram without having to code their own bot.

All these solutions are designed for all types of businesses, ranging from startups to SMEs and enterprises.

Revenue Model: All the ChangeNOW white-label fintech solutions come at an affordable price and with a revenue-share model from different streams. For instance, in the white-label crypto wallet, you earn an exchange commission of 0.4% on the transactions made via your business. And the good thing? The fee for transactions can be changed and customized for specific assets/pairs/exchange flows upon request.

You can also earn staking rewards of up to $3,000 per 1 BTC staked via the wallet and an interest on every loan issued (example: $3,600 for every 1 BTC loaned).

Customization Options: When integrated with a ChangeNOW white-label, you can tweak colors, branding, flow, and even the assets that appear, so your exchange, wallet, or bot feels yours.

Ease of Integration: Integration with any of the ChangeNOW white-label solutions is flexible. For the exchange and wallet solutions, integration is available via a ready-to-deploy widget or an API, which gives you deeper control and a more tailored experience. For the white-label telegram bot, all you have to do is reach out via [email protected] to get the source code and create your bot in BotFather.

The best thing is that at each stage of integration, ChangeNOW will always answer all your questions and can also provide a personal account manager.

NOWPayments

Overview:NOWPayments is a payment gateway platform that offers a white-label fintech solution for businesses to accept payments in over 350 cryptocurrencies. The platform also offers automatic conversion between crypto and fiat currencies, allowing your business to easily expand its payment options and attract more users.

In terms of custody, the platform has a flexible model based on businesses’ operational needs. They can either receive payments directly in their own wallets or utilize NOWPayments’ custody features for easier fund management and payouts. This way, a business can launch crypto capabilities faster, cheaper, and with complete brand control.

Revenue model: NOWPayments operates on a pay-as-you-go revenue model. This means there are no service fees for integration, support, or further account optimization. Their revenue is primarily generated from a standard 0.5% service fee that you pay for every transaction they process for your customers.

If you use autoconversion, where, for example, you accept one crypto like BTC but want the payment settled in another currency like USDT, the fee increases to 1%. The good thing is that you can choose to deduct these fees from your business profit or have customers pay them.

The platform also has an affiliate program that grants you 25% of the net profit they make from every transaction made by merchants you refer to them. NOWPayments also recently launched a new mass payouts flow with 0 network and service fees and settlement speeds of up to 1 second for ecosystem wallets via ChangeNOW Pro.

Customization Options: NOWPayments allows your businesses to build fully custom payment and payout experiences, 100% under your domain and design. They deliver a fully invisible integration where your customers see only your interface, logo, and flows, while they handle all transaction processing, settlement, and compliance in the background.

Ease of Integration: Integration of the payment gateway is made quick and effortless through their comprehensive API documentation, available in 13 programming languages. Additionally, NOWPayments offers a customizable payment button that can be easily added to any website for instant cryptocurrency transactions.

Finally, the platform's team is always there to guarantee that you are never alone on the integration journey.

Rapyd

Overview: Rapyd is a company offering white-label solutions fintech services that enable businesses to collect payments in local currencies, conduct payouts, and maintain digital wallets globally through a white-label solution. The platform operates across 100+ jurisdictions and allows businesses like e-commerce websites, neobanks, and payroll companies to support 900+ payment methods and more than 65 currencies.

Along with these integrated finance capabilities, it also offers card issuing, fraud protection, and identity management services.

Revenue model: Rapyd’s primary revenue is generated by charging a percentage on each transaction and a foreign exchange (FX) fee. As a business using its payment gateway, you pay a percentage per transaction plus a fixed fee, which varies by country and payment method. FX fees also apply to cross-border transfers.

For your business, revenue is earned from recurring commissions based on processed transaction volume through a tiered program. And because the transaction fee is fixed, as a merchant, you are free to optimise your pricing strategy; for example, you could adjust the prices based on your region to capture the margin.

Customization Options: As a partner or merchant, you can fully customize the user interface of Rapyd to align with your needs. This entails modifying the custom theme file, font, screen logo, and more. The platform also supports plugins that allow you to instantly connect hundreds of local payment methods to your shopping cart to incorporate customer-preferred options.

Ease of Integration: Integration with the white-label is done through Rapyd's REST API. The platform also offers a comprehensive suite of documents and team support to help with this.

Gemba

Overview: Gemba is a no-code white-label fintech platform based in London that provides a full-stack embedded finance platform for non-bank businesses. One of the platform's core strengths is speed, where businesses can launch a white-label banking app in under seven minutes.

The platform also supports a comprehensive range of payment rails, including FPS, BACS, CHAPS, SWIFT, SEPA, and Target2, which make it suitable for both domestic UK payments and international transactions. Its model also allows any technology company to embed banking services without obtaining its own financial license.

Revenue model: Gemba has zero setup fees and a quite generous revenue model where partners retain up to 70% of the revenue on custom fees they set for end users, plus a 20% share of base transaction fees.

Customization Options: The platform has tailored solutions installed quickly to match your brand identity and business requirements. As a partner, you upload branding, configure a color palette, and map the application to your own subdomain via a self-service portal.

Ease of Integration: Integration of the banking feature is made easy by a simple and easy installation process requiring just a few DNS record setups. This means instead of a complex software installation, you essentially 'point' your web address to their pre-built banking system.

Crassula

Overview: Crassula offers a fintech white-label software solution that provides digital banking capabilities to fintech businesses across Europe. It comes with a complete suite of financial infrastructure components, including multi-currency accounts, card issuing, SEPA and SWIFT payments, onboarding flows, compliance orchestration, foreign exchange, and crypto wallets.

This infrastructure is designed to support any business model to build their own banking services, or what we call Banking as a Service (BaaS). All this can be delivered to your business in 10 business days in a budget-friendly manner.

Revenue model: Crassula operates on a SaaS (Software-as-a-service) subscription model, which means businesses pay a recurring monthly or annual subscription fee to access the platform. On top of this, they pay low usage fees per active account/user or per transaction (starting around $0.03/month).

To generate revenue as a business, integrating its solution, you set your own price lists for end-users in transaction fees, monthly subscriptions, or FX markups. Essentially, you pay for the tech and own the profit.

Customization Options: The solution comes customized with your color scheme, logos, and brand style. And if you go for the apps, you get both iOS, Android, and Web apps that look and feel like your own.

Ease of Integration: Integration on Crassula follows a modular-based approach, with each model tailored for specific businesses. The first one is the no-code white-label UI, which allows businesses to connect their domains with its pre-built web and mobile apps via DNS settings. The other one is through REST API, which gives businesses deeper integration control and a more tailored experience.

AlphaPoint

Overview: AlphaPoint targets the institutional end of the market. This is the kind of white-label fintech solution that should come to mind if you want to run a real exchange with order books, serious volumes, and long-term plans for scaling. It serves over 35 countries and can process nearly 1 million transactions per second, which puts it comfortably in enterprise territory.

Beyond facilitating trading, the white-label comes with the capabilities to allow your users to tokenize real-world assets through Polymesh. Its payment processing tools support crypto-to-fiat conversion and debit card use through Visa and Mastercard. While it takes more effort to set up the solution, once you succeed, you get an infrastructure that is meant to support professional trading rather than just basic swap flow.

Revenue model: AlphaPoint operates on a B2B enterprise licensing and usage model. You pay a fixed operational cost to rent the exchange technology. To generate revenue for your business, you configure your own platform fees for trading, liquidity spreads, withdrawals, or deposits. The good thing is that you retain 100% of the profits from these fees.

Customization Options: The platform supports a customizable UX/UI, which allows businesses to fully adjust both front-end and back-end features, aligning interfaces, market settings, and trading thresholds with their specific goals.

Ease of Integration: Integration is API-based (both REST and WebSocket), which means you can connect it with your payment providers, internal systems, and external services without rebuilding an entire stack.

SDK.finance

Overview: SDK.finance provides two white-label solutions: a PSP (Payment Service Provider) software that delivers payment software for businesses that need to build or expand a payment gateway and a digital banking software meant to provide businesses with everything they need to launch a digital bank. The two solutions support neobanks, digital wallets, payment gateways, and crypto-fiat rails and are available in two models: SaaS for a fast and cost-efficient start and a source code license for full ownership and unlimited customization.

One of SDK.finance’s strongest values lies in its ability to support high transaction throughput of up to 2,700+ TPS.

Revenue model: SDK.finance's revenue model is based on subscriptions from the two models. The SaaS model requires a recurring monthly subscription fee of €5,500 plus a fixed per-transaction fee of €0.05. The Source Code, on the other hand, only requires a one-time purchase through a direct project quote, and it provides full ownership of the platform’s codebase.

As a business integrating the platform, your revenue is generated from custom trading fees, withdrawal charges, and currency exchange spreads you charge your customers in your own system. The good thing is that you retain 100% of these fees.

Customization Options: Customization is also based on the model. The SaaS model comes with pre-built web UI and iOS/Android mobile apps. Source Code on the other end offers unlimited customization where you can tailor SDK.finance to fit your unique business needs by modifying existing functionalities or adding new ones.

Ease of Integration: SDK.finance white-label software comes with pre-built integrations. New integrations can be added either by the team on request or by developers using the platform’s 470+ API endpoints.

Swan

Overview: Swan is a Banking-as-a-Service provider built primarily for European tech companies that want to embed accounts, cards, and payments into their existing product. Through its white-label solution, companies can launch banking products without obtaining their own licence or establishing relationships with sponsor banks.

Its infrastructure includes KYC/KYB orchestration, AML screening, card issuing through Mastercard, and building dashboards for transaction oversight. The platform provides both virtual and physical cards, which helps it support many consumer and business banking use cases.

Revenue model: Swan has fixed subscription costs and a partnership sharing revenue structure. First, the platform charges a flat monthly fee, which starts from 2990€. On top of this, there are small fixed costs for specific actions like account opening, card issuance, and transactions.

In terms of revenue sharing, the platform gives you a percentage of the fees collected from your customers and sets your own 'price list' for end-users. For example, if they charge you €1 for a specific service, you can charge your customer €2 and pocket the €1 margin.

Customization Options: All Swan’s banking products are customizable to meet your business and customer desires. This ranges from physical cards, payment channels, and accounts.

Ease of Integration: Integrating the banking service is done through a GraphQL API with ready documents and a team to guide you.

Conclusion

Launching a fintech product no longer requires building every piece of infrastructure from scratch; through white-label fintech products, your business can access ready-made financial systems and customize them to match its brand. And with the solutions above, choosing the right one for your business should not be a problem. If you are looking to integrate banking services, Gemba, Crassula, SDK.finance, and Swan offer the best option for you. And if you are an institution looking to offer full exchange functionalities, AlphaPoint has you covered.

But don't forget, if you are looking to integrate swap or exchange functionalities into your product, ChangeNOW white-label provides the best option for you.

This article compares the 12 best developer-friendly crypto APIs for Web3 products in 2026. It explains what each API helps teams build, from embedded swaps and RPC access to market data, NFT tools, payments, wallet connectivity, and decentralized storage.

Multichain fragmented liquidity and turned asset movement into a bottleneck, making bridges core execution infrastructure rather than a supporting layer. This piece analyzes leading protocols based on how they handle liquidity, fees, and speed under real cross-chain conditions.